Rolling one-step ahead forecasts of Value at Risk and Expected Shortfall

rollcast.RdComputes rolling one-step ahead forecasts of Value at Risk and Expected Shortfall (Conditional Value at Risk) by means of plain historical simulation age- and volatility-weighted historical simulation as well as filtered historical simulation.

Arguments

- x

a numeric vector of asset returns

- p

confidence level for VaR calculation; default is

0.975- model

model for estimating conditional volatility; options are

'EWMA'and'GARCH'; ifmodel = 'GARCH', additional arguments can be adjusted via...; default is'EWMA'- method

method to be used for calculation; default is

'plain'- lambda

decay factor for the calculation of weights; default is

0.98formethod = 'age'and0.94formethod = 'vwhs'ormethod = 'fhs'- nout

number of out-of-sample observations; most recent observations are used; default is

NULL- nwin

window size for rolling one-step forecasting; most recent observations before out-of-sample are used; default is

NULL- nboot

size of bootstrap sample; must be a single non-NA integer value with

nboot > 0; default isNULL- smoothscale

a character object; defines the smoothing approach for the unconditional variance from the logarithm of the squared centralized returns; for

smoothscale = 'lpr', the unconditional variance is smoothed via thesmoots::gsmooth()function from thesmootspackage; the bandwidth has to be chosen manually; otherwise the default is used; ifsmoothscale = 'auto', the functionsmoots::msmooth()is employed and the bandwidth is chosen automatically (data-driven); see the documentation of thesmootspackage for more information; is set tosmoothscale = 'none'by default- smoothopts

additional arguments of

smoots::gsmooth()andsmoots::msmooth(); see the documentation of thesmootspackage for more information; is set to customized default settings- ...

additional arguments of the

ugarchspecfunction from therugarch-package; only applied ifmodel = 'GARCH'; default settings for the argumentsvariance.modelandmean.modelare:variance.model=list(model = 'sGARCH', garchOrder = c(1, 1))mean.model=list(armaOrder = c(0, 0))

Value

Returns a list with the following elements:

- VaR

Numerical vector containing out-of-sample forecasts of Value at Risk

- ES

Numerical vector containing out-of-sample forecasts of Expected Shortfall (Conditional Value at Risk)

- xout

Numerical vector containing out-of-sample returns

- p

Confidence level for VaR calculation

- model

Model for estimating conditional volatility

- method

Method to be used for calculation

- nout

Number of out-of-sample observations

- nwin

Window size for rolling one-step forecasting

- nboot

Size of bootstrap sample

Examples

prices <- DAX$price.close

returns <- diff(log(prices))

n <- length(returns)

nout <- 250 # number of obs. for out-of-sample forecasting

nwin <- 500 # window size for rolling forecasts

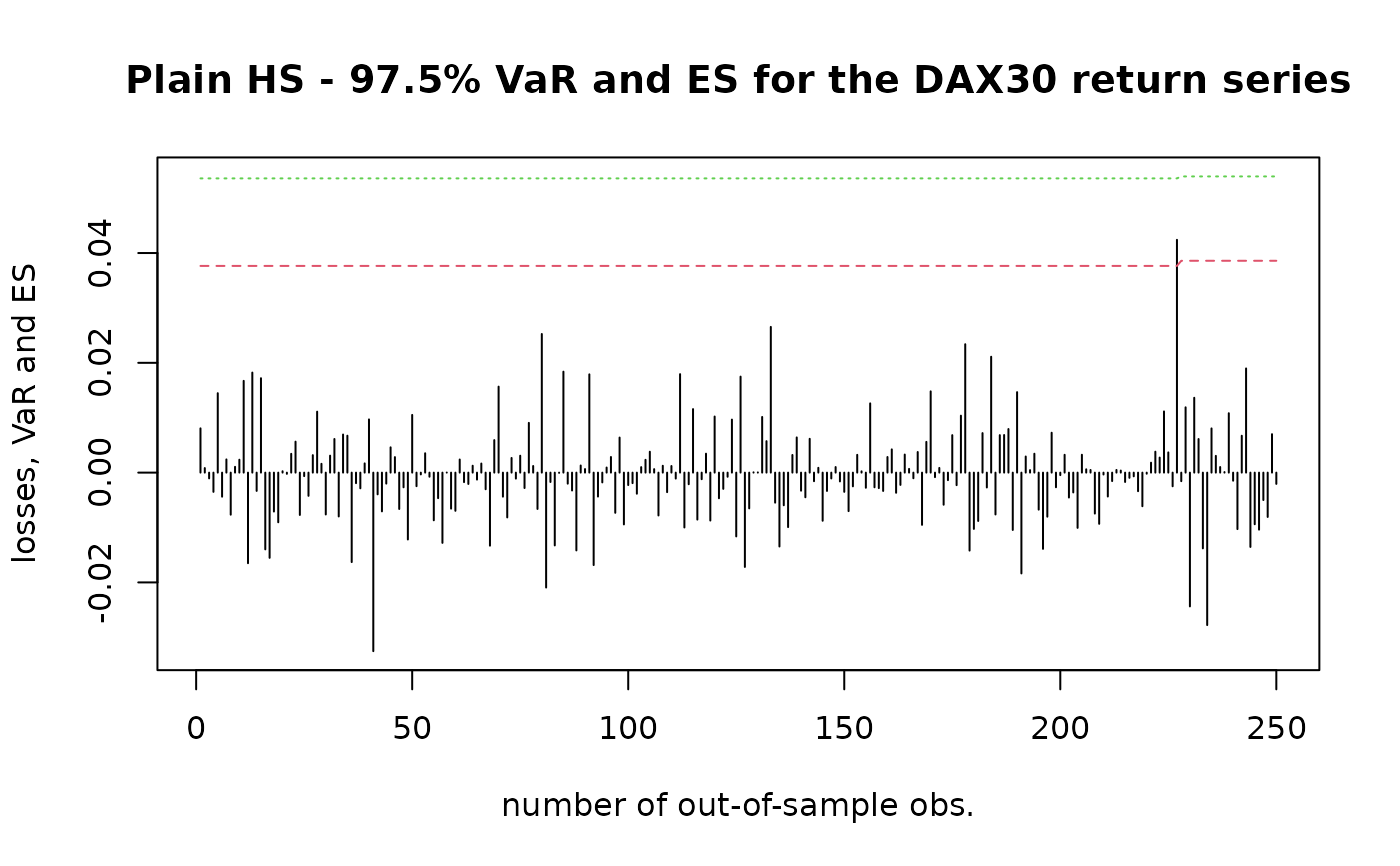

### Example 1 - plain historical simulation

results1 <- rollcast(x = returns, p = 0.975, method = 'plain', nout = nout,

nwin = nwin)

#>

#> Calculations completed.

matplot(1:nout, cbind(-results1$xout, results1$VaR, results1$ES),

type = 'hll',

xlab = 'number of out-of-sample obs.', ylab = 'losses, VaR and ES',

main = 'Plain HS - 97.5% VaR and ES for the DAX30 return series')

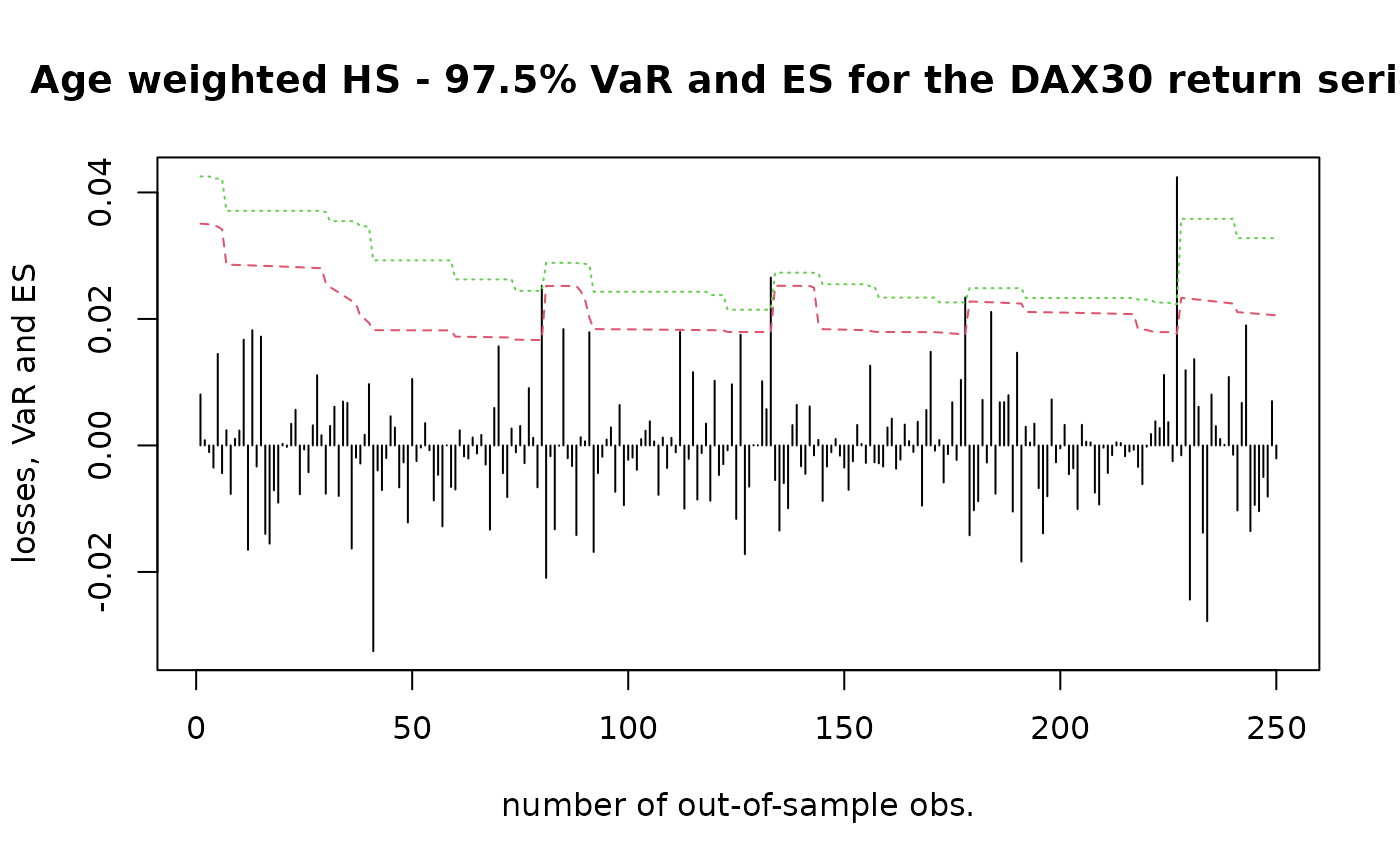

### Example 2 - age weighted historical simulation

results2 <- rollcast(x = returns, p = 0.975, method = 'age', nout = nout,

nwin = nwin)

#>

#> Calculations completed.

matplot(1:nout, cbind(-results2$xout, results2$VaR, results2$ES),

type = 'hll',

xlab = 'number of out-of-sample obs.', ylab = 'losses, VaR and ES',

main = 'Age weighted HS - 97.5% VaR and ES for the DAX30 return series')

### Example 2 - age weighted historical simulation

results2 <- rollcast(x = returns, p = 0.975, method = 'age', nout = nout,

nwin = nwin)

#>

#> Calculations completed.

matplot(1:nout, cbind(-results2$xout, results2$VaR, results2$ES),

type = 'hll',

xlab = 'number of out-of-sample obs.', ylab = 'losses, VaR and ES',

main = 'Age weighted HS - 97.5% VaR and ES for the DAX30 return series')

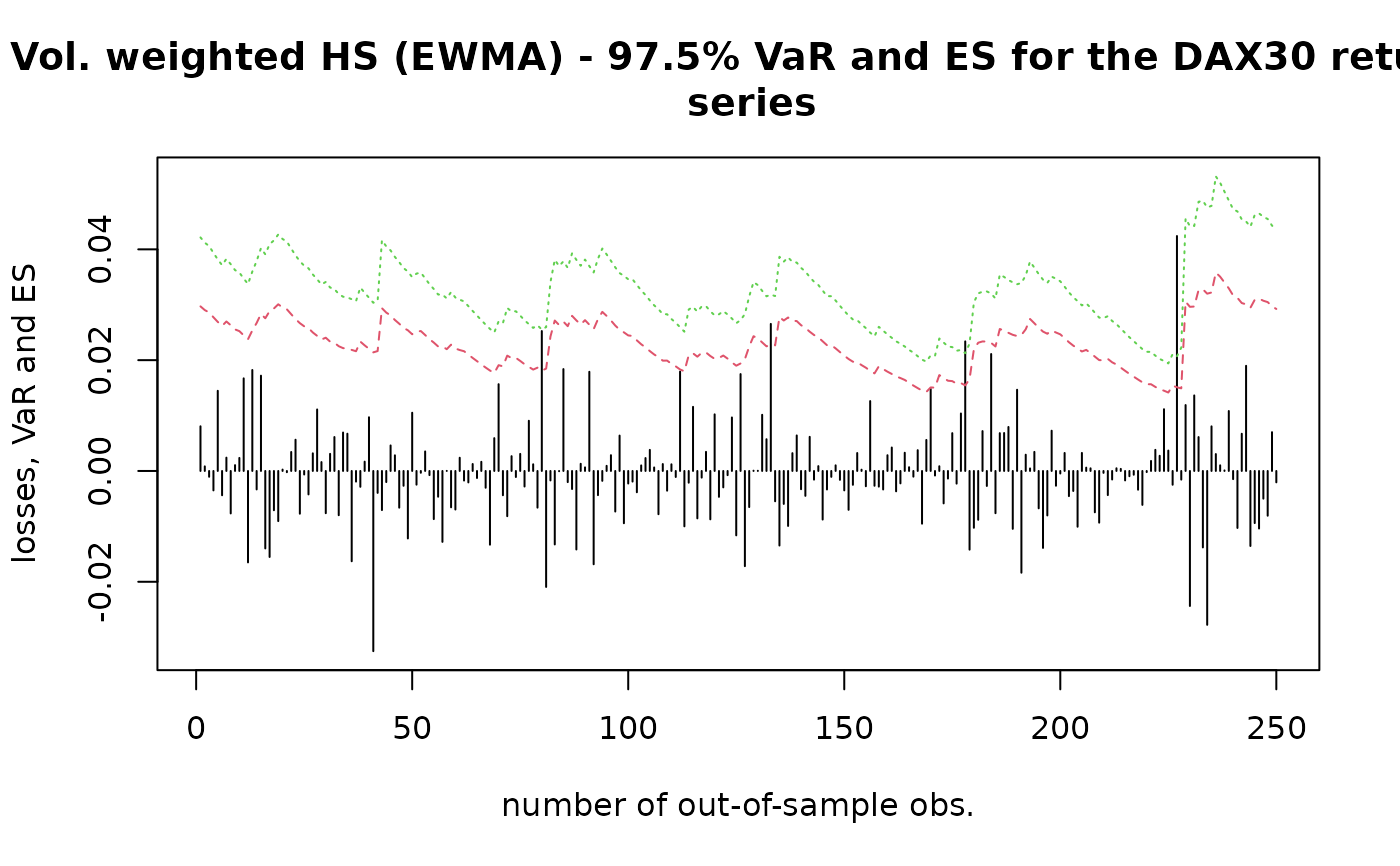

### Example 3 - volatility weighted historical simulation - EWMA

results3 <- rollcast(x = returns, p = 0.975, model = 'EWMA',

method = 'vwhs', nout = nout, nwin = nwin)

#>

#> Calculations completed.

matplot(1:nout, cbind(-results3$xout, results3$VaR, results3$ES),

type = 'hll',

xlab = 'number of out-of-sample obs.', ylab = 'losses, VaR and ES',

main = 'Vol. weighted HS (EWMA) - 97.5% VaR and ES for the DAX30 return

series')

### Example 3 - volatility weighted historical simulation - EWMA

results3 <- rollcast(x = returns, p = 0.975, model = 'EWMA',

method = 'vwhs', nout = nout, nwin = nwin)

#>

#> Calculations completed.

matplot(1:nout, cbind(-results3$xout, results3$VaR, results3$ES),

type = 'hll',

xlab = 'number of out-of-sample obs.', ylab = 'losses, VaR and ES',

main = 'Vol. weighted HS (EWMA) - 97.5% VaR and ES for the DAX30 return

series')

# \donttest{

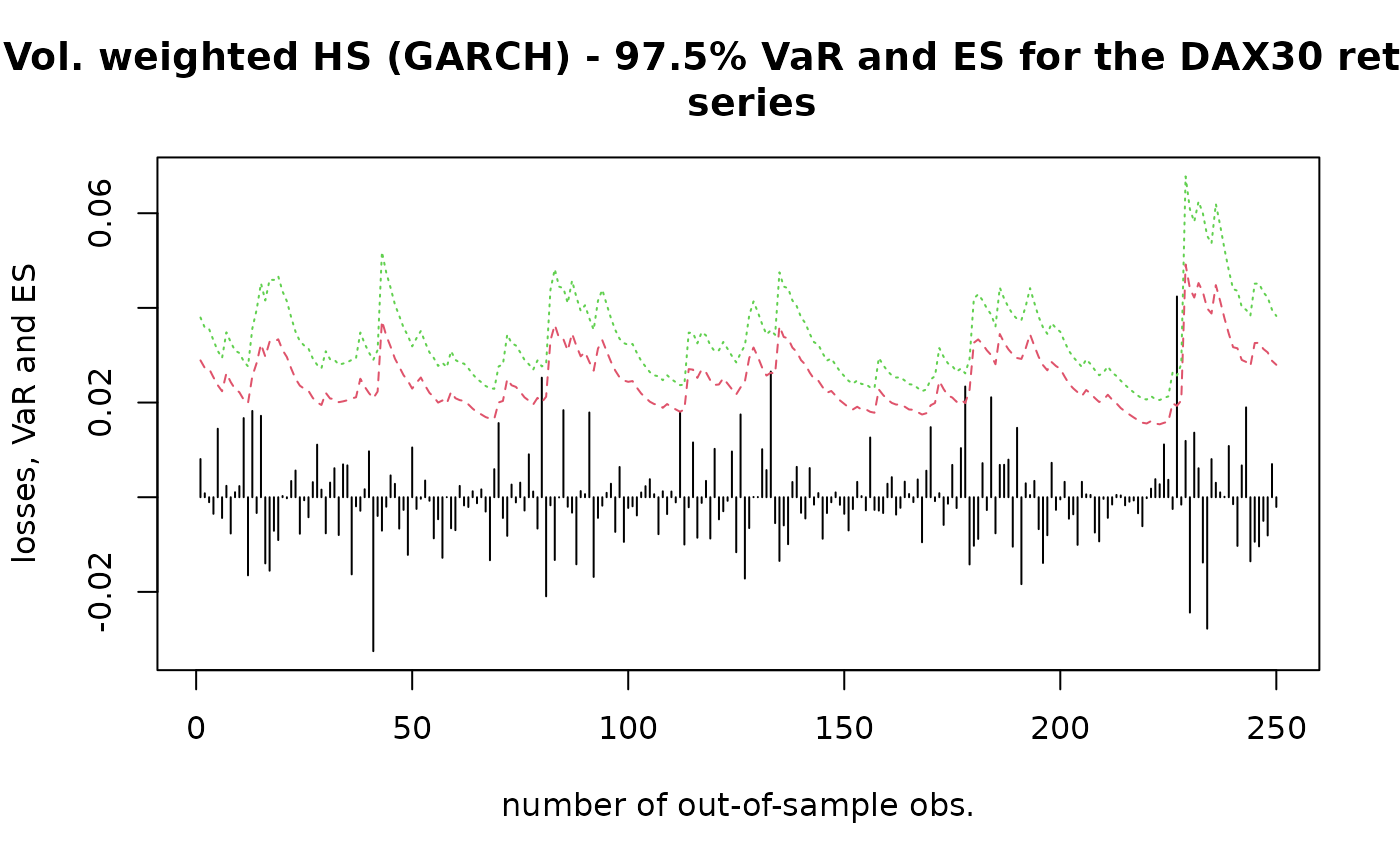

### Example 4 - volatility weighted historical simulation - GARCH

results4 <- rollcast(x = returns, p = 0.975, model = 'GARCH',

method = 'vwhs', nout = nout, nwin = nwin)

#>

#> Calculations completed.

matplot(1:nout, cbind(-results4$xout, results4$VaR, results4$ES),

type = 'hll',

xlab = 'number of out-of-sample obs.', ylab = 'losses, VaR and ES',

main = 'Vol. weighted HS (GARCH) - 97.5% VaR and ES for the DAX30 return

series')

# \donttest{

### Example 4 - volatility weighted historical simulation - GARCH

results4 <- rollcast(x = returns, p = 0.975, model = 'GARCH',

method = 'vwhs', nout = nout, nwin = nwin)

#>

#> Calculations completed.

matplot(1:nout, cbind(-results4$xout, results4$VaR, results4$ES),

type = 'hll',

xlab = 'number of out-of-sample obs.', ylab = 'losses, VaR and ES',

main = 'Vol. weighted HS (GARCH) - 97.5% VaR and ES for the DAX30 return

series')

# }

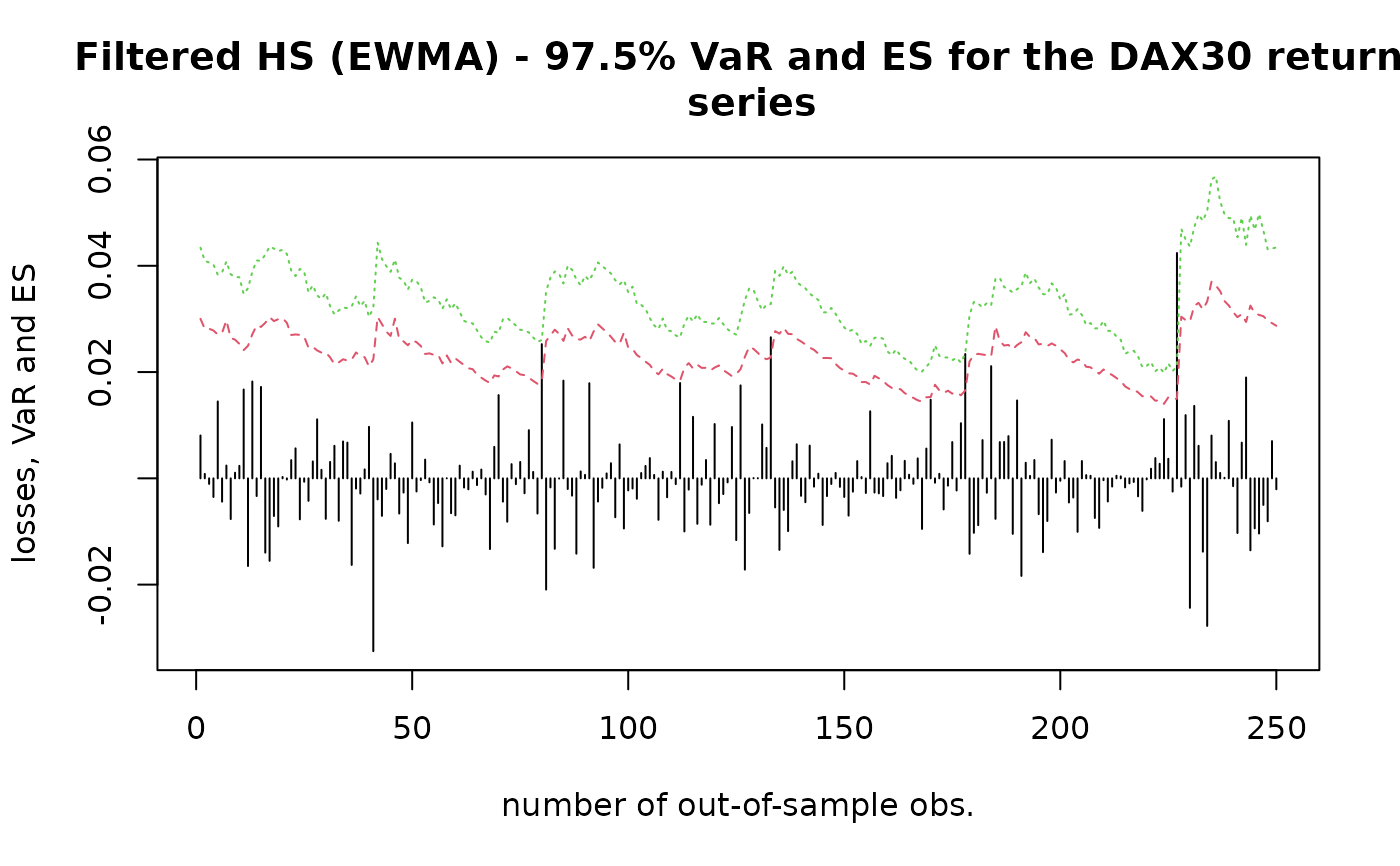

### Example 5 - filtered historical simulation - EWMA

results5 <- rollcast(x = returns, p = 0.975, model = 'EWMA',

method = 'fhs', nout = nout, nwin = nwin, nboot = 10000)

#>

#> Calculations completed.

matplot(1:nout, cbind(-results5$xout, results5$VaR, results5$ES),

type = 'hll',

xlab = 'number of out-of-sample obs.', ylab = 'losses, VaR and ES',

main = 'Filtered HS (EWMA) - 97.5% VaR and ES for the DAX30 return

series')

# }

### Example 5 - filtered historical simulation - EWMA

results5 <- rollcast(x = returns, p = 0.975, model = 'EWMA',

method = 'fhs', nout = nout, nwin = nwin, nboot = 10000)

#>

#> Calculations completed.

matplot(1:nout, cbind(-results5$xout, results5$VaR, results5$ES),

type = 'hll',

xlab = 'number of out-of-sample obs.', ylab = 'losses, VaR and ES',

main = 'Filtered HS (EWMA) - 97.5% VaR and ES for the DAX30 return

series')

# \donttest{

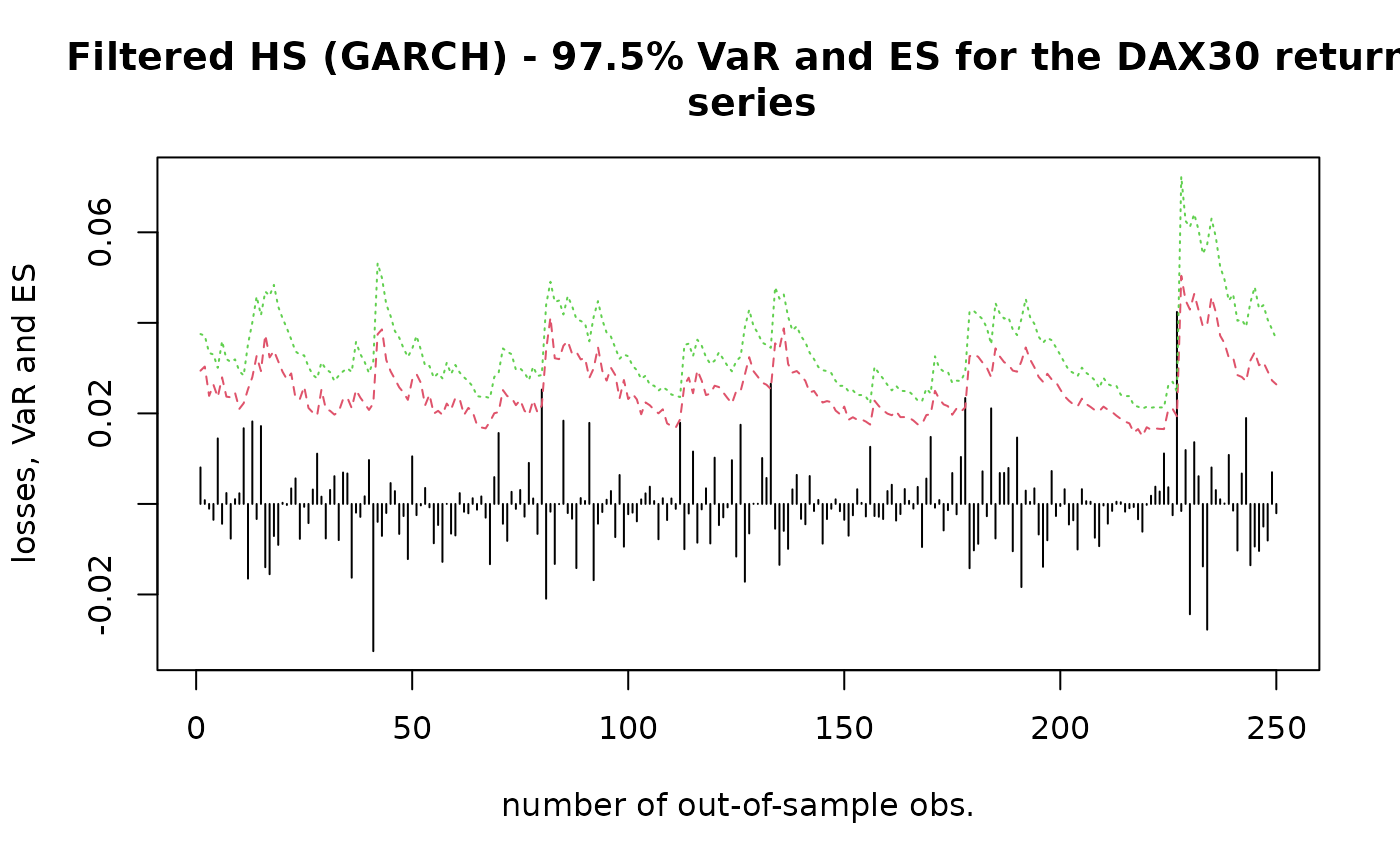

### Example 6 - filtered historical simulation - GARCH

results6 <- rollcast(x = returns, p = 0.975, model = 'GARCH',

method = 'fhs', nout = nout, nwin = nwin, nboot = 10000)

#>

#> Calculations completed.

matplot(1:nout, cbind(-results6$xout, results6$VaR, results6$ES),

type = 'hll',

xlab = 'number of out-of-sample obs.', ylab = 'losses, VaR and ES',

main = 'Filtered HS (GARCH) - 97.5% VaR and ES for the DAX30 return

series')

# \donttest{

### Example 6 - filtered historical simulation - GARCH

results6 <- rollcast(x = returns, p = 0.975, model = 'GARCH',

method = 'fhs', nout = nout, nwin = nwin, nboot = 10000)

#>

#> Calculations completed.

matplot(1:nout, cbind(-results6$xout, results6$VaR, results6$ES),

type = 'hll',

xlab = 'number of out-of-sample obs.', ylab = 'losses, VaR and ES',

main = 'Filtered HS (GARCH) - 97.5% VaR and ES for the DAX30 return

series')

# }

# }